IAS 36 - Reversing impairment losses

06 May 2022Step 6 of applying the guidance in IAS 36 as set out in our article ‘Insights into IAS 36 – Overview of the Standard’ relates to recognising or reversing and impairment losses. This article focuses on part of this step; reversing impairment losses. For recognising impairment losses refer to our article ‘Insights into IAS 36 – Recognising impairment losses’.

IAS 36 ‘Impairment of Assets’ sets out the requirements to follow prior to concluding if and when an asset should be impaired. However, due to the complex nature of the Standard, the requirements of IAS 36 can be challenging to apply in practice.

The articles in our ‘Insights into IAS 36’ series have been written to assist preparers of financial statements and those charged with the governance of reporting entities understand the requirements set out in IAS 36, and revisit some areas where confusion has been seen in practice.

Indicators for reversing an impairment loss

In addition to assessing evidence of possible impairment, entities must also assess whether there is any indication a previously recognised impairment loss for an asset (other than goodwill) no longer exists or the assessed impairment amount may have decreased. If an indication of possible reversal is identified, the entity must estimate the recoverable amount of that asset.

|

Guidance note: Goodwill impairment cannot be reversed IAS 36 prohibits any reversal of impairment losses recognised on goodwill. The reason for this is because IAS 36 views any increase in the recoverable amount of goodwill after the recognition of an impairment loss to likely be an increase in the internally generated goodwill (not a reversal of the impairment loss recognised for the acquired goodwill). IAS 38 ‘Intangible Assets’ prohibits the recognition of internally generated goodwill. Accordingly, the references to impairment reversals in this article do not include goodwill. |

Similar to the list provided in IAS 36 indicating when there might be an impairment loss, the Standard also provides a nonexhaustive list of circumstances when a previously recognised impairment loss may no longer exist. These are summarised below.

Non-exhaustive list of impairment reversal indicators from IAS 36

External sources of information:

- Observable indications that the asset’s value has increased significantly during the period

- Significant favourable changes (have occurred or are expected) in the technological, market, economic or legal environment

- Market interest rates or other market rates of return on investments have decreased during the period (which will decrease the discount rate used in caluclating the asset’s value in use (VIU))

Internal sources of information

- Significant favourable changes (have occurred or are expected) in the extent to which an asset is used (or is expected to be used) (eg, costs incurred during the period to improve or enhance the asset’s performance or restructure the operation to which the asset belongs)

- Evidence is available from internal reporting that indicates the economic performance of an asset is, or will be, better than expected.

The reversal of an impairment loss reflects an increase in the estimated service potential of an asset (either from use or from sale) since the date when an entity last recognised the impairment loss for the asset. A reversal of an impairment loss should therefore only be recognised if there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognised. Said differently, an impairment loss is not reversed solely because of the passage of time or the unwinding of the discount, even if the recoverable amount of the asset becomes higher than its carrying amount.

|

Guidance note: Disclosure required for an increase in the estimated service potential

|

Regardless of whether an impairment loss is reversed for an asset, if the entity identifies an indication a previously recognised impairment loss may no longer exist, the entity may need to review and adjust the:

- the remaining useful life

- the depreciation (amortisation method), and/or

- the residual value of the asset.

Practical insight – Indicators for reversing a previously recognised impairment loss

Most of the ‘reversal indicators’ listed are the inverse of the loss indicators listed in IAS 36 (discussed in ‘Insights into IAS 36 – If and when to test for impairment’); there are however some exceptions to this. In particular, an increase in market capitalisation above carrying value of an entity’s net assets is not listed as a reversal indicator.

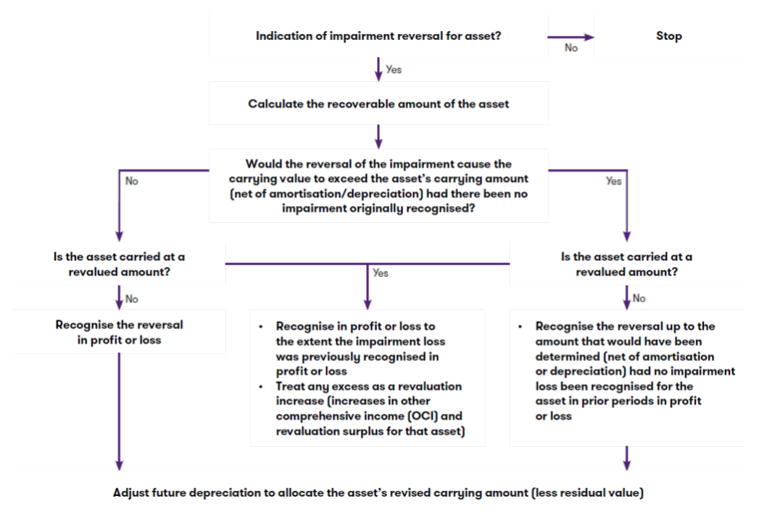

Reversing impairment losses for individual assets (other than goodwill)

When recoverable amount is recalculated and exceeds the asset’s carrying value, the carrying amount is increased to the recoverable amount subject to a ‘ceiling’ (ie an upper limit). The increased carrying amount cannot exceed the carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior years.

For assets accounted for using the revaluation model in IAS 16 ‘Property, Plant and Equipment’ or IAS 38, the reversal of the impairment loss is accounted for in the same way as a revaluation increase in accordance with those standards.

The diagram below depicts the requirements for reversals of impairment losses for individual assets and the following example illustrates their practical application.

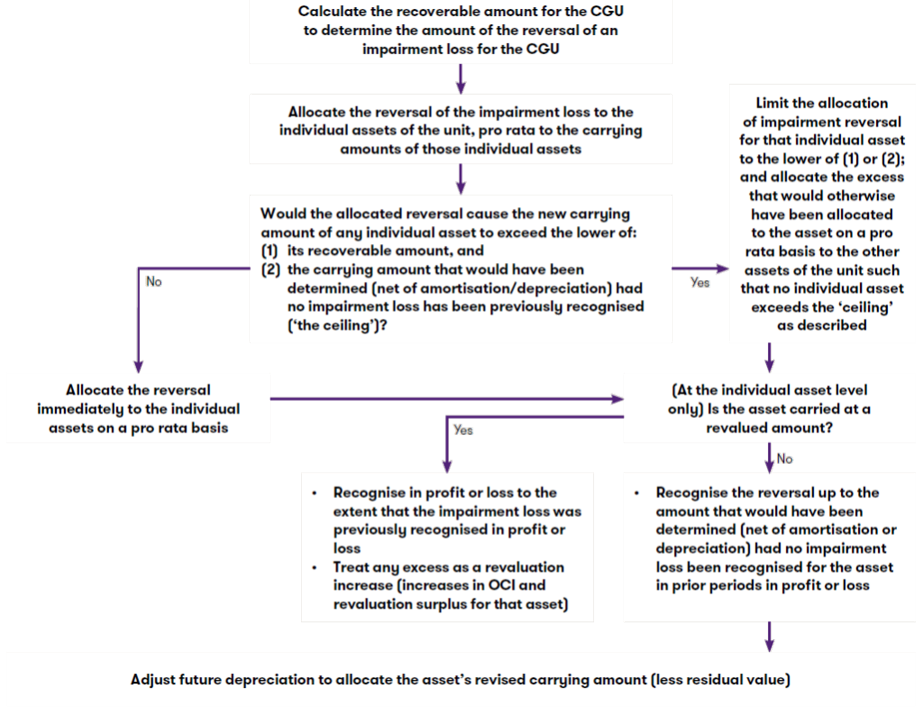

Reversing impairment losses for cash-generating units

Any reversal of an impairment loss for a cash-generating unit (CGU) must be allocated to the individual assets that make up the CGU (excluding goodwill). The entity is required to allocate the reversal of an impairment loss to the CGU’s assets pro rata to their carrying amounts. This is again however subject to a ‘ceiling’ whereby no individual asset’s carrying amount is increased above the lower of:

- its recoverable amount (if determinable), and

- its carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior periods.

If this ‘ceiling’ takes effect for one or more of the CGU’s assets, the reversal of the impairment loss that would otherwise have been allocated to those assets is allocated on a pro rata basis to the other assets, subject to the same ceiling.

The below flowchart depicts the allocation process.

Download the full Reversing impairment losses article for an example of reversing a previously recognised impairment loss for an individual asset and an example that illustrates the practical application of the requirements.

How we can help

We hope you find the information in this article helpful in giving you some insight into IAS 36. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact our related expert.